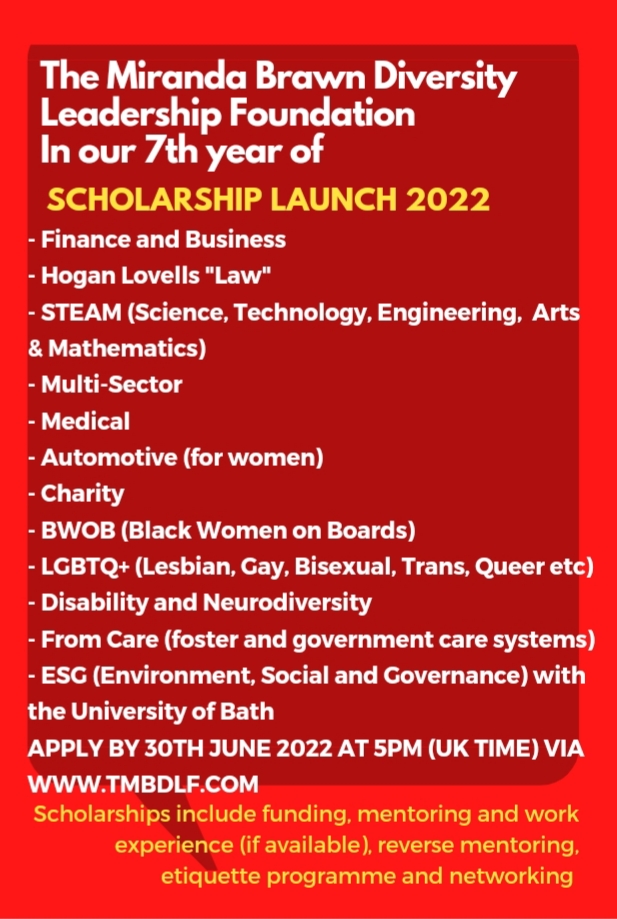

Applications for The Miranda Brawn Diversity Leadership Scholarships 2022/23 now open

PRESS RELEASE: 1ST MARCH 2022

The Miranda Brawn Diversity Leadership Foundation (TMBDLF)’s scholarship application process opened on 1st March 2022.

The mission of this registered charity is to eliminate the diversity, equity and inclusion gaps in the professional workplace by educating, empowering and inspiring out next generation of diverse student leaders. The aim is to make a real difference in the lives of our next generation by giving them a ticket to the lottery of life.

There are at least 12 scholarships available to young people up to ages of 30 years from diverse backgrounds. Set up on the 4th January 2016, this is The Miranda Brawn Diversity Leadership Foundation (TMBDLF)’s seventh year.

Applicants must be at school, college or university on a full-time basis and achieving good grades with an interest in diversity. Applications close on 30th June 2022 at 5pm (London time).

The scholarship award includes £500 to £1,000 in funding, mentoring and reverse mentoring with leaders in their field, work experience (if available and pending COVID restrictions) with leading UK organisations, etiquette educational training, networking, graduation group mentoring lunch and VIP ticket to the annual diversity leadership lectures. More information on the scholarship programme is available via TMBDLF’s website https://www.tmbdlf.com/scholarship-programme.

The categories include Finance and Business, Hogan Lovells ‘Law’, STEAM (Science, Technology, Engineering, Arts and Mathematics), Multi-Sector, Medical, Automotive (for women), Charity, BWOB (Black Women on Boards), LGBTQ+ (Lesbian, Gay, Bisexual, Transgender, Queer etc), Disability and Neurodiversity, From Care (foster and government care systems), ESG (Environment, Social and Governance) with the University of Bath.

Each year we launch new innovative scholarships. This year has included a scholarship called ‘Automotive (for women)’ to celebrate International Women’s Month 2022 and our ESG scholarship has re-launched this year with a University of Bath partnership as part of the One Young World Bath Caucus. Other new innovative scholarships this year include Charity, From Care and Neurodiversity.

A full list of categories and eligibility are also available online. To apply visit the Charity’s website www.tmbdlf.com

The winners will be announced at The Miranda Brawn Diversity Leadership Annual Lecture Event 2022 which will take place later this year in the UK. The date and venue will be confirmed in due course. Further details will be shared on the website by summer 2022. https://www.tmbdlf.com/annual-lecture-and-events

For more information, to support and/or apply for a scholarship, please email TMBDLF’s team directly via info@tmbdlf.com.

Founder Dr Miranda K. Brawn with the Miranda Brawn Diversity Leadership Winners for 2021 at TMBDLF Graduation Group Mentoring Lunch and Etiquette Programme Launch Event held in September 2021 at the Bluebird Restaurant in Chelsea, London UK.

SPAC vs IPO

After more than a decade of buildup, special purpose acquisition companies (SPACs) have exploded and are gaining momentum in the US and beyond.

Special purpose acquisition companies (SPACs) were big news in 2020, breaking records and captivating markets and media alike.

SPACs raised a record US$82.4 billion in 248 US IPOs in 2020, data from Dealogic shows. This compares with US$13.5 billion for 59 IPOs in 2019. In addition, 92 SPACs announced business combinations in 2020, with a total deal value of US$151 billion, up from 27 SPACS with a total deal value of US$27.6 billion in 2019.

Despite sponsor and investor interest from around the globe, SPACs have primarily been a US phenomenon. That may be changing—the London Stock Exchange is weighing possible rule changes to encourage SPAC listings; Nasdaq updated its rules to enable SPAC listings in Stockholm, effective February 1, 2021; and SPAC offerings are in process on Euronext in various European countries.

What Is a Special Purpose Acquisition Company (SPAC)?

A special purpose acquisition company (SPAC) is a company with no commercial operations that is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company. Also known as “blank check companies”. SPACs have been around for decades. In recent years, they have become more popular, attracting big-name underwriters and investors and raising a record amount of IPO money in 2019. In 2020, as of the beginning of August, more than 50 SPACs have been formed in the U.S. which have raised some $21.5 billion.

What is an IPO and how does it work?

An initial public offering (IPO) refers to the process of offering shares of a private corporation to the public in a new stock issuance. Public share issuance allows a company to raise capital from public investors.

What is the purpose of an IPO?

Companies typically issue an IPO to raise capital to pay off debts, fund growth initiatives, raise their public profile, or to allow company insiders to diversify their holdings or create liquidity by selling all or a portion of their private shares as part of the IPO.

Are SPACs better than IPOs?

Private companies are flocking to SPAC deals for a few big reasons. One is that a typical SPAC comes with a 2% underwriter fee and 3.5% fee at completion compared with 7% for a traditional IPO. The timeline of a SPAC is usually three to four months versus up to a year with a traditional IPO.

How does a SPAC IPO work?

A SPAC raises capital through an initial public offering (IPO) for the purpose of acquiring an existing operating company. Subsequently, an operating company can merge with (or be acquired by) the publicly traded SPAC and become a listed company in lieu of executing its own IPO.

How does a SPAC work?

This is the same as a SPAC IPO. SPACs are generally formed by investors, or sponsors, with expertise in a particular industry or business sector, with the intention of pursuing deals in that area. In creating a SPAC, the founders sometimes have at least one acquisition target in mind, but they do not identify that target to avoid extensive disclosures during the IPO process. (This is why they are called “blank check companies.” IPO investors have no idea what company they ultimately will be investing in.) SPACs seek underwriters and institutional investors before offering shares to the public.

The money SPACs raise in an IPO is placed in an interest-bearing trust account. These funds cannot be disbursed except to complete an acquisition or to return the money to investors if the SPAC is liquidated. A SPAC generally has two years to complete a deal or face liquidation. In some cases, some of the interest earned from the trust can be used as the SPAC’s working capital. After an acquisition, a SPAC is usually listed on one of the major stock exchanges.

Advantages of a SPAC

Selling to a SPAC can be an attractive option for the owners of a smaller company, which are often private equity funds. First, selling to a SPAC can add up to 20% to the sale price compared to a typical private equity deal. Being acquired by a SPAC can also offer business owners what is essentially a faster IPO process under the guidance of an experienced partner, with less worry about the swings in broader market sentiment.

SPACs Make a Comeback

SPACs have become more common in recent years, with their IPO fundraising hitting a record $13.6 billion in 2019—more than four times the $3.2 billion they raised in 2016. They have also attracted big-name underwriters such as Goldman Sachs, Credit Suisse, and Deutsche Bank.

Examples of High-Profile SPAC Deals

One of the most high-profile recent deals involving special purpose acquisition companies involved Richard Branson’s Virgin Galactic. Venture capitalist Chamath Palihapitiya’s SPAC Social Capital Hedosophia Holdings bought a 49% stake in Virgin Galactic for $800 million before listing the company in 2019. In 2020, Bill Ackman, founder of Pershing Square Capital Management, sponsored his own SPAC, Pershing Square Tontine Holdings, the largest-ever SPAC, raising $4 billion in its offering on 22 July.

Hot Sectors

A number of sectors in particular stood out in 2020.

Online gaming

Online gaming has been very active, with several transactions hitting the market in addition to DraftKings. These include the US$3.5 billion transaction between Flying Eagle Acquisition Corp. and Skillz Inc., the US$1.4 billion transaction between dMY Technology Group, Inc. and Rush Street Interactive, LP, and the US$800 million transaction between Landcadia Holdings II, Inc. and Golden Nugget Online Gaming, Inc.

Automotive – Electric Vehicle (EV) and Automotive Technology

The automotive sector, particularly electric vehicle manufacturers and automotive technology, has also been hot. Notable deals include Velodyne Lidar, which announced in early July its plan to merge with the SPAC Graf Industrial Corp. in a deal that valued the combined entity at US$1.8 billion. Velodyne is a supplier of lidar (light, detection and ranging) technology for developers of autonomous vehicles. The deal closed in October.

Life sciences

Life sciences has also been very active, with a number of SPACs launched by life sciences-focused investment funds.

SUMMARY

- A special purpose acquisition company (SPAC) is formed to raise money through an initial public offering to buy another company.

- At the time of their IPOs, SPACs have no existing business operations or even stated targets for acquisition.

- Investors in SPACs can range from well-known private equity funds to the general public.

- SPACs have two years to complete an acquisition or they must return their funds to investors.

ESG Investing, the Electric Vehicle (EV) Automotive industry and SPAC / IPO

Electric Car and Bus Markets

What is ESG?

ESG stands for “environment, social and governance”.

What is ESG Investing?

ESG investing entails researching and factoring in environmental, social, and governance issues, in addition to the usual financials, when evaluating potential stocks for portfolios. Research is increasingly showing that this investing method can reduce portfolio risk, generate competitive investment returns, and help investors feel good about the stocks they own.

There are any number of ways for investors and business leaders to explore the EV or ESG conversation right now. The push for sustainable options in every sector reaches well beyond the automotive industry. The next generation consumer and market intelligence ensures you will see those trends coming and be ready to adapt (or adopt) early.

Electric Vehicles Are The Future

Until recently, mass adoption of Electric Vehicle (EV) technology has been concentrated primarily in the small vehicle category, targeted at reducing the numbers of the highly polluting two- and three-wheelers ubiquitous in Asia’s cities. Through a system of subsidies to encourage mass adoption of these EVs, China has sought to improve air quality throughout its many bustling city-centres.

Policies encouraging adoption of more sustainable behaviours are beginning to shift from incentivising consumers to regulatory enforcement, although the economic impact of COVID-19 has resulted in countries temporarily prioritising economic recovery. Furthermore, pressure to conform to more socially responsible practices is becoming increasingly mainstream.

Whilst China has led adoption of EVs and battery technology in recent years, European consumers and manufacturers are now rapidly turning to EVs, catalysed by incentives seeking to boost economic activity. EVs are generally regarded as ‘green’ technology, however the supply of mineral ingredients for batteries is likely to give rise to new sustainability challenges.

Regulations to Replace Subsidies

Regulations put in place by the Chinese government have increasingly focused on encouraging consumers and manufacturers to switch away from polluting ICEs to cleaner EV technology. Since 2019, China’s vehicle manufacturers have been incentivised to produce and sell greater volumes of their EVs through a system of credits for each unit produced, reflecting factors such as type, energy consumption, weight and range. Manufacturers that do not achieve agreed sales targets must either purchase credits from competitors or face financial penalties.

This subsidy system – introduced in 2012 as part of a push to reduce air pollution in China’s cities – has successfully stimulated EV adoption in the country. However, whilst the system was scheduled to be phased out in 2020, the combined impact of weaker-than-expected EV sales in 2019 and the shock of COVID-19 has meant that the withdrawal of purchase tax exemptions has been deferred until 2022.

The European Union’s 2014 Directive required member states to set targets for public recharging infrastructure; in 2017 it established the Battery Alliance, aimed at fostering co-operation between member states, industry and the European Investment Bank. As the EU has developed its environmental and sustainability policies, a combination of strategic support and regulatory pressure has been developed; for example, in 2019 stakeholders were consulted on how to use regulations to rapidly foster a battery market that provides high quality, cost efficient and competitive products in a sustainable manner.

Adoption

Battery technology limitations have until recently meant high uptake has been limited above all to smaller vehicles, with approximately 350 million two- and three-wheeled EVs in use worldwide, representing 25% of all vehicles in this category globally. Use of these light vehicles has been centred primarily in Chinese cities, although adoption is spreading to other highly-populated cities in India and ASEAN nations.

Electrification of urban bus fleets is also seen as an area of potential growth, as their short routes and driving cycles are compatible with contemporary battery limitations. Globally, there are around half a million electric buses in use, about half of which are in Chinese cities. Extra-urban buses and lorries, however, do not readily lend themselves to electrification due to long distances and charging infrastructure requirements – today’s battery technology simply do not possess the range to make uptake in this sector viable for now.

Electric car global sales in 2019 amounted to 2.1 million, taking the global stock of electric cars to 7.2 million; or 2.6% of global car sales and 1% of global car stocks. As China experienced weak demand continuing into 2020 because of the COVID-19 pandemic, sales in Europe increased significantly, up by 57% in the first half of 2020, even as the overall trend of vehicle sales volumes showed a significant dip (down 37%). This change was mainly in response to European countries introducing new economic recovery schemes targeting green technology, taking European sales volumes ahead of China for the first time.

Automakers are rapidly growing their product ranges while shifting away from plug-in hybrids (PHEVs). In 2019, 143 new EV models were launched, while a further 450 models are expected by 2030, mostly consisting of mid-sized and large vehicles. Although the number of manufacturers and models is rapidly expanding, Tesla retains quite remarkable leadership. In the first half of 2020, global sales of the Tesla Model 3 amounted to 142,000 vehicles while the second most popular EV, the Renault Zoe, achieved a reduced 38,000 unit sales.

McKinsey estimates that by 2030 EVs could account for 20% of global vehicle sales, whereas Deloitte anticipate significant regional variations, with China making up 48% of total sales, Europe 27% and US only 14%.

One of the factors effecting adoption rates is the oil price, as consumers are highly sensitive to costs relative to ICE vehicles. The International Energy Agency calculates an oil price of US$25 per barrel will increase the payback period by 1 – 2.5 years compared to oil price of US$60. Fuel tax policy is also an influence; in countries such as Germany with 60% fuel tax, there is greater incentive to switch away from internal combustion engines than in the US where tax is around 20%.

EV growth rates are expected to slow beyond 2030, as wealthy countries will have substantially adopted the technology as far as is practical. In poorer countries, adoption will be slower due to the significant capital requirements to construct charging infrastructure necessary to make day-to-day use feasible.

New Money

Rare earth miners and uranium producers have enjoyed the flood of new money going into electric vehicles and environmental, social, and governance investment themes as reported by Bloomberg. Lithium producers have traditionally benefited from the growth in the electric vehicle market and the broader green energy push that has raised demand for lithium-ion batteries. More recently, rare earth producers have also gained momentum amid the greater push toward electric vehicles, especially with the Biden administration targeting a zero-emission future more reliant on clean energy alternatives.

There is an accelerating adoption of electric vehicles and electrification trends in wind turbines. Rare earth metals are incorporated in new technologies, from lithium-ion batteries to electric vehicles, wind turbines, and missile guidance systems. There is also limited global supply as only a handful of producers globally produce the metals.

Uranium stocks are now gaining attention from ESG investors due to their low GHG footprint and quintessential role as a clean energy alternative, the set-up for incremental/new Uranium investments as opportune for greenhouse gas emissions.

Young Investors are attracted to the Electric Vehicle market

With new apps available making investing an attainable option for anyone, young investors are increasingly attracted to the electric vehicle market – and to the surrounding conversation. Capturing customer experiences analytics with social listening is critical, as their investment decisions mirror their buying habits. Next generation consumer and market intelligence is key. Millennials love electric vehicles.

Electric Vehicles Batteries

The demand for EV batteries is expected to soar as automakers increasingly comply with emission standards and boost their production of battery electric vehicles (BEVs), according to a new report from Moody’s Investor Service. Tightening regulations and growth of BEVs are also expected to spur improvements in battery capacity. The International Energy Agency projects global battery capacity for BEVs and plug-in hybrid vehicles will grow by 24% on a compounded annual basis between 2020 and 2030.

Top makers of EV batteries, including Contemporary Amperex Technology, LG Chem, Panasonic Corporation and SK Innovation are set to benefit from rising demand. These four account for more than half of global production. However, a sharp rise in production will pose operational risks and increase the challenge of keeping leverage ratios stable, according to the report. As battery makers invest in emerging technology, strong relationships with automakers will be critical for their credit quality.

Makers of EV batteries who maintain solid relationships with automakers that have a clear strategy to expand BEV sales will see their revenue and profit stay stable. Among the four rated battery makers, Amperex Technology’s margin will remain the highest and stay around low double-digits over next 12 to 18 months, thanks to high-capacity utilization and China’s EV subsidies. In comparison, other battery makers’ margins are single-digit or less, according to the report.

Battery Technology

McKinsey estimate the cost of an EV to be made up primarily of the battery pack, accounting for a full 40%-50% of the price while the power train represents another 20%. Lithium-ion (Li-ion) batteries commonly used in EVs presently use cathodes (a negatively charged electrode that’s the source of electrons generating the electrical charge) made from three mineral mixtures, with nickel cobalt aluminium oxide (NCA), nickel manganese cobalt oxide (NMC) and lithium iron phosphate (LFP) being the most prominent.

NMC, however, is the most widely used type due to its energy density properties. Energy density, or the amount of energy held in the battery per unit weight, is highly prized in many EV markets and is largely defined by the nickel content of the battery; this will likely represent one of the ways in which performance will be improved over coming years. On the other hand, it is worth noting that not all batteries are manufactured to optimise energy density. Other considerations such as cost or size constraints may be more important so that usage specifications vary; small battery packs are most common in Asia, whilst in Europe and US batteries are larger.

In the years since 2010, battery costs have fallen from US$1,000 kWh to US$147 kWh. Bloomberg New Energy Finance expects these will fall to around US$100 in 2023/4 and US$61 by 2030. It has been reported that Tesla is now working with Chinese battery manufacturer CATL on LPF battery technology which could reduce costs below the US$100 per kWh mark, helping to achieve cost parity with ICEs.

Sustainability

Recycling regulations primarily focus on making battery manufacturers responsible for waste through the entire life-cycle until scrapped, referred to as Extended Producer Responsibility (EPR). Batteries are also recycled by converting used packs for lower specification EVs, or reconfigured as part of electrical storage facilities.

In China, companies are mainly focused on recycling materials in preference to repurposing used batteries, in response to regulations and shortages in supply of lithium, 85% of which is imported. In 2020 the EU brought forward new regulations intended to protect and improve the environment by minimising adverse impacts of batteries through prohibiting certain materials and requiring battery producers to take responsibility for end collection and recycling. In the US, waste regulation is primarily set at the state level, with certain states having introduced battery recycling and disposal laws, while others have applied EPR principles.

While EVs are effective in reducing harmful air pollutants, large scale use of minerals such as cobalt and nickel bring their own challenges. High quality nickel, one of the main components of modern batteries, is extracted from rock containing just 1% of usable material. Such high quantities of waste product are potentially a major environmental concern; with increased demand its expected production will shift from Canada and Australia to Indonesia, where mining firms will have to sustainably dispose of large volumes of waste to ensure Indonesia’s seas with their rich coral reefs and turtles are not endangered.

Regulation, Technology and Investments

Impressive statistics on the rollout of electric vehicles (EVs) are the result of regulation, technological improvements, and greater investment in EV supply chains. But accessible, efficient, and low-cost charging infrastructure remains a prerequisite for widespread EV adoption; deploying this infrastructure efficiently and achieving target return rates will be more complex than immediately apparent.

Highlighting the magnitude of the transformation required to manage climate change, there is a commitment to cut net carbon emissions to zero within the next few decades. Zero-carbon transport is just one of the requirements for achieving this goal. Immense changes to power generation, heating, agriculture, and manufacturing will also be required.

Biggest Tech Breakthrough in a Generation

The early investors in the new type of device that experts say could impact society as much as the discovery of electricity. Current technology will soon be outdated and replaced by new devices. In the process, it is expected to create 22 million jobs and generate $12.3 trillion in activity.

Charging points

Charging points are a vital aspect of the overall shift towards the electrification of transport. Various forecasts put the number of EVs on UK roads at between two and six million by 2030. EV drivers will seek to have residential chargers installed in their homes wherever that is an option: around 57% of UK households currently park on a driveway or in a domestic garage. Technical guidance from the EU recommends one public charger per 10 electric vehicles. This means hundreds of thousands of public chargers will be needed to enable the expected deployment of EVs, an exponential rise from the current level of roughly 20,000.

Competition to install the charging points is already intensifying as early entrants seek to gain advantage and capture market share. Car makers increasingly see the provision of ancillary services as paving the way for vehicle sales growth. Energy companies are increasingly looking to diversify their fossil-fuel exposure too, while utilities see synergies with their traditional energy-supply businesses. Finally, independent specialists have emerged who are seeking to capture market share and provide solutions for corporate clients such as shopping malls, supermarkets, fleet operators, and large employers.

The residential charging market is attractive to EV installers due to its large size and growth prospects. It is becoming increasingly commoditised, though, with low barriers to entry enabling increased competition and pressuring margins. Achieving economies of scale will be the key challenge for developers in this market segment.

On the other hand, public charging networks – particularly rapid charging – feature higher barriers to entry and potentially more stable revenues in the future. Location is crucial for this: some places, such as motorway service stations, have a more stable base of captive users than others like carparks or retail and leisure locations. Low utilisation is the main challenge for these assets, as preliminary data suggest around 80-90% of charging is conducted at home. Rapid chargers are seldom used even in markets such as Norway, where the EV transition is well under way. Furthermore, fast public charging can require significant upfront investment, not least in power network upgrades.

The good news for investors is that EV adoption is intensifying and creating a large market for the build out of ancillary infrastructure. Clarity on user behaviour and competitive dynamics will develop over the next five to 10 years. In the meantime, investors in charging infrastructure will need the patience to develop an in-depth understanding of consumer behaviour, the interaction between location and utilisation, and a tolerance for risk.

Electric Bus and Public Transportation Market

The electric bus market size exceeded $28 billion in 2020 and is expected to grow at 11% compound annual growth rate (CAGR) between 2021 and 2027. The market is forecast to grow at an exponential rate due to the rapid increase in uptake of electric buses as a sustainable mode of transport according to a new report by Global Market Insights (GMI).

Electric buses are primarily operated by the integrated electric batteries. This also includes plug-in hybrid buses and fuel-cell electric buses. The report says stringent emission regulations and directives imposed by governments across the globe will propel the adoption of electric buses. In 2019, France announced its 100% zero-emission vehicle target for 2040. As a part of the Paris Climate agreement, the country passed a law to ban ICE vehicle sales by 2040.

Electric buses are 100% eco-friendly as they operate on electrically-powered engines. They do not release smoke or toxic gases into the environment as they operate on a clean energy obtained from battery packs. Several benefits of electric buses, such as low maintenance costs and reduced pollution by emissions, are augmenting their representation in the market.

The increasing focus of several countries, such as India, China, and Canada, on promoting electrification of public transport is providing lucrative growth opportunities, according to GMI. Initiatives undertaken by several governments to reduce the carbon footprint of public transportation are boosting the electric bus market size through 2027.

The electric bus industry alongside every other industry has been impacted by the prevailing situations of COVID-19. The manufacturing of electric buses has been affected and sales numbers also decreased because of mass quarantines and lockdown during the first two quarters of 2020. Industry players have faced challenges on account of shortage of capital and financial insecurities caused by the decline in revenues. However, the market is expected to witness steady growth subject to the revival of global economic conditions in 2021, supported by policy changes and government support.

SPAC Merger Became the Trendiest EV IPO Route of 2020

The demand for electric vehicles (EVs) is fueling on the back of climate change concerns, favourable government policies and superior technologies. Investors are intrigued by automakers that look for solutions to lower global carbon emissions for providing a cleaner energy future. With green vehicles striking the right chord with investors, it has been raining IPOs in the EV market during the past year. Seemingly, merger with special purpose acquisition companies (SPACs) turned out to be the most popular course of action for an EV IPO in 2020.

What is a SPAC?

SPACs, or blank-check companies, are shell vehicles that raise money to take a private company public via a reverse merger. Unlike traditional initial public offerings (IPOs), SPAC deals allow listing candidates to market financial projections to investors, a perk for earlier stage companies that have yet to prove their business model.

SPACs have changed the traditional IPO market. SPACs are flourishing in the EV market, helping startups to avoid the complexity and strenuous paperwork associated with the traditional IPO. Many EV companies chose to go public in 2020 via reverse mergers with SPACs, a faster, simpler and less demanding process than the conventional means of making a debut on the stock market.

Electric-vehicle companies, many of which are yet to launch commercial products, have taken advantage of that. Nikola Corp was the first high profile one to go public via a SPAC listing, followed by others including Lordstown Motors Corp, Fisker Inc and Canoo Inc. U.S. listings have dominated the SPAC boom, but Europe’s stock exchanges are now catching up. The IPOX SPAC Index tracks the performance of a broad group of blank-check companies.

Conclusion

The early stages of adoption by users of medium and large cars has commenced, with higher sales volumes shifting from China to Europe. At present, volumes of battery-powered EV sales are small as a proportion of global vehicle sales, although rapidly rising; Tesla retains leadership and dominates the mid- and large-sized EV market. Higher levels of adoption are expected in wealthier nations where the significant cost of recharging infrastructure can be financed.

Governments around the world are embracing EVs as a green technology that reduces harmful air pollutants and are putting regulations in place which make battery manufacturers responsible for their products throughout their entire lifecycle. As consumers become more aware of the environmental impact of their actions and governments face growing liabilities from air pollution, adaption in many countries is now regarded as a necessity rather than a lifestyle choice.

Additionally, merger with special purpose acquisition companies (SPACs) has good prospects to continue with the 2020 popularity course of action for an EV IPO.

With the election of President Biden, who has signalled his commitment to sustainability by rapidly moving to re-join the Paris Agreement and appointing John Kerry as the special envoy on climate change, there is now the prospect the US will join China and Europe in forcing further change.

SFDR – New ESG challenges for the UK

What is SFDR?

The Sustainable Finance Disclosure Regulation (SFDR) is part of the European Commission’s package of reforms to implement its sustainable finance strategy. The strategy focuses on three areas:

- Strengthening the foundations for sustainable investment by creating an enabling framework. The Commission believes many financial (and non-financial) companies still focus excessively on short term financial performance instead of long-term development and sustainability-related challenges and opportunities.

- Increasing opportunities to have a positive impact on sustainability for citizens, financial institutions and corporates – enabling them to “finance green”.

- Integrating climate, environmental, and social risks into financial institutions and the financial system as a whole.

To that end SDFR introduces a series of disclosure requirements for investment firms to address environmental, social and governance (ESG) concerns. It applies to asset and fund managers (e.g. MiFID investment managers, alternative investment fund managers (AIFMs), and UCITS managers), and investment firms, as well as credit institutions and insurers. The SFDR entered into force in December 2019 and its implementation date is on 10 March 2021.

How does it apply to UK firms?

The UK government has opted not to implement the SFDR into UK domestic law following the end of the UK’s Brexit transition period. However, SFDR will most likely still be relevant for UK firms either as a requirement under the regulation or in practical terms. For example, if a UK-based private equity firm wants to market into the EU or manage EU-based funds, it will be subject to the SFDR in its capacity as an Alternative Investment Fund Manager (AIFM). Additionally, we are likely to see firms complying with the SFDR for commercial reasons, particularly due to client or investor pressure

Even if a UK firm does not have to comply with the SFDR, the UK government plan to put green finance high on its agenda. In November 2020, UK Chancellor Rishi Sunak announced the government’s plans for the financial services sector ahead of the end of the Brexit transition period. The plans included the introduction of “more robust environmental disclosure standards so that investors and businesses can better understand the material financial impacts of their exposure to climate change, price climate-related risks more accurately, and support the greening of the UK economy”.

A HM Treasury spokesperson said: “[Last] year the Chancellor announced the UK’s intention to be the first G20 country to make disclosures that are aligned with the recommendations of the Task Force on Climate Related Financial Disclosures fully mandatory across the economy by 2025, going beyond the “comply or explain” approach adopted under the SFDR. We are considering the requirements for legislation relating to the SFDR and will set out further details in due course.”

For asset managers, the Financial Conduct Authority (FCA) is consulting in H1 2021 on potential TCFD-aligned client disclosure rules, aimed at providing ESG information at the firm, fund, and portfolio level to aid decision-making for investors. The UK regime is therefore likely to overlap substantially with SFDR.

What changes will SFDR bring?

The SFDR disclosure requirements involve a number of potentially challenging compliance hurdles for firms to overcome. There is a requirement to disclose “principal adverse impacts” (PAIs) of investment decisions on sustainability factors on a “comply or explain” basis. PAIs are defined as impacts of investment decisions and advice that result in negative effects on sustainability factors. The key challenge will be the collection of data. Firms will need to collect data from various sources, then map that data into a singular and robust data model. Data quality checks and transparency will be important compliance factors. Challenges like these will be costly and time consuming.

At the very least, firms now should be getting up to speed with the SFDR and the related Taxonomy Regulation and understanding where they fall within the scope of the regulation and what changes that will entail to their current practice. In light of the requirements, firms should start reviewing marketing materials and website disclosures. Firms should prepare their position on PAIs. If PAIs are voluntary then firms may wish to implement a phased approach, whereby they explain in March 2021 that they are not ready to disclose against the rules but will be reporting later in the year.

Firms should not wait to start making implementation plans. Client and investor demand remains a key developing driver of ESG changes and firms need to make headway in this area or risk being left behind.

The text of the SFDR can be viewed here.

Summary

The EU’s regulation on sustainability disclosures in the financial services sector, also known as the SFDR, came into effect on 10 March 2021. The UK government has elected not to implement the regulation in legislation since Britain left the EU’s regulatory umbrella at the beginning of 2021. However, the UK government is considering implementing similar rules. Advisers should also consider following SFDR regulation as good practice, even if it is not UK law because the regulation could be an example of good practice and a competitive advantage.

It will be key to understand clients’ ESG requirements and to research innovative solutions. While the government chose not to implement the SFDR, the regulation would apply to advisers if they have clients living in Europe, according to adviser trade body Pimfa. Those with only UK clients, meanwhile, would not have to apply the regulation.

The UK government is due to introduce its own version of the SFDR but there is currently no information on when that will be, whether it will simply mirror the SFDR or if it will differ in certain ways.

The expectation is that it will be at least one year before the UK will launch its own version of the SFDR so the requirement(s) around sustainable finance is still some way off.

The rules would have required advisers to ask clients about sustainability preferences in their suitability checks as part of the advice process. They also require financial advisers to publish on their websites information about how they integrate sustainability risks into their investment or insurance advice.

TCFD recommendations

The Climate-related Financial Disclosures (TCFD or Task Force) recommendations are designed to solicit consistent, decision-useful, forward-looking information on the material financial impacts of climate-related risks and opportunities, including those related to the global transition to a lower-carbon economy.

Governance

Disclose the organisation’s governance around climate-related risks and opportunities.

Strategy

Disclose the actual and potential impacts of climate-related risks and opportunities on the organisation’s businesses, strategy, and financial planning where such information is material.

Risk Management

Disclose how the organisation identifies, assesses, and manages climate-related risks.

Metrics and Targets

Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

ESG and SDG Investing in Latin America and the Caribbean

Latin America and the Caribbean are increasingly relying on environmental, social and governance, or ESG, investments to help address their financial needs. The region faces an infrastructure gap and has recently seen financial institutions withdraw, in part due to the region’s vulnerability to natural disasters and climate change. While some financial institutions have withdrawn from the region, according to the Climate Bond Initiative, Latin America and the Caribbean saw an increase in the green bond markets in 2019, contributing to 2 percent of green bonds issued globally. With oil and gas markets hitting record lows, the region and global investors may use this opportunity to shift their focus to sustainable and green investments.

With the arrival of the Covid-19 pandemic, ESG in Latin America and the Caribbean is needed now more than ever, offering a potential growing market for investors looking at the space. Specifically, Covid-19 revealed gaps in infrastructure globally, including in Latin America and the Caribbean. Pandemic-response bonds are already emerging and are designed to deal with the social and economic repercussions of Covid-19. It would seem that at this point in time, Latin America and the Caribbean present a unique market for ESG investment. Indeed, the region, once heavily associated with corruption, has increased anti-corruption efforts, in part to increase global investment and make the region more inviting to investment dollars on projects other than the exploitation of natural resources. Companies are eager to boast ethically conscious and socially responsible investments in an effort to differentiate themselves and receive attention from international investors.

Latin America, like anywhere else, has companies that care about ESG issues and others that do not. It is important to understand what lens you are looking at ESG through: are you an investor or asset manager, or are you the company’s board and c-suite overseeing and implementing an ESG strategy? Any way you look at it, ESG has arrived globally—especially in the investor community—and cannot be ignored locally or regionally by any company. ESG is here to stay and even more so because of the global disruption Covid-19 has wreaked.

There are two key factors in whether a company is ESG responsive: 1.) how enlightened and responsible leadership and the board are on these issues, or how superficial, greenwashing-oriented or downright irresponsible they are; and 2.) how committed, proactive or outright activist key stakeholders are—especially investors but also communities, customers, NGOs, suppliers, regulators and employees. Additionally, the seriousness with which ESG is taken also depends on the sector and how immediately exposed that sector is to ESG.

Latin America

Thus, a company in the mining and extractive industry will or should be much more attuned to environmental and social issues than most (though these also interconnect directly with good, mediocre or poor governance, as we have seen in several notorious scandals in Latin America—Petrobras, Odebrecht, Vale). While other sectors may think they do not have a strong ESG remit or profile, they should think again—for example, the rise of ESG awareness is especially strong in the investor and asset management community globally. Add to the mix we already had pre-Covid-19 (for example, climate change), additional pandemic-induced systemic changes such as supply chain disruption, social and racial inequality, popular unrest, health care and economic failures potentially on a massive scale.

Now more than ever is the time for both investors and issuers in Latin America to adopt and fully integrate an ESG agenda as part of their daily business, long-term strategy for value creation, resilience and sustainability. It is a matter of survival, not just competitive advantage, to do so.

ESG has been a growing theme for private capital investors in Latin America over the last decade, with fund managers dedicating new resources to monitor and measure the social and environmental impact of their investments.

Since 2014, LAVCA has been tracking deal cases with important environmental, social, governance and gender outcomes. These examples are wide-reaching and range from traditional impact sectors such as financial inclusion and renewable energy to businesses in consumer/retail, IT, agribusiness, financial services, health care, education, real estate and infrastructure. In addition, there have been a number of traditional fund managers co-investing alongside those with an impact-only mandate in Latin America, indicating that there is an appetite and opportunity to invest in companies and projects that yield tangible social and environmental objectives across sectors and countries. Correlated to an increasing limited partner/general partner focus on climate change, investment in clean tech, alternative and renewable energies in Latin America has gone from $470 million invested across 35 deals in 2014-2016 to $2 billion across 63 deals in 2017-2019, according to LAVCA Industry Data.

Climate change and environmental considerations have never been more prominent in investment conversations across emerging markets. More than three-quarters of commercial limited partners (LPs) participating in the latest EMPEA LP survey on emerging markets private capital cited taking such factors into account when making investment decisions. While most LPs do not yet face specific restrictions on their allocation choices, a multitude of factors—including pressure from boards and beneficiaries and increasing evidence of ESG’s role in positive investment outcomes—has generated significant momentum behind sustainable investing. One family office said, “In recent years, we have been actively divesting our public stock portfolio in developed markets to increasingly focus on private capital in emerging markets for social/charitable purposes.’ With a shift in priorities becoming even more obvious in the current world scenario, we are seeing investors better understand their role in maintaining the long-term sustainability of global markets by way of responsible investing.”

Caribbean

Good governance is a major concern in the Caribbean. Indeed, the issue of corruption is an ongoing point of discussion in some countries and a topic that tends to arise during elections. This was amply evident during 2020 voting in the Dominican Republic, Guyana, Suriname, and Trinidad and Tobago. In each case, campaign narratives included citizens’ concerns over governance, which impact their day-to-day lives in the form of quality of public services, accountability of government finances, and law and order.

While the need for better governance is an issue in the Caribbean, the region is hardly unique in dealing with such challenges. Caribbean governments are finding themselves increasingly brought into a broader international system of governance accountability. While at times this may be perceived as external interference, the creation of such a global accountability regime generally functions as a force for positive change, especially if it contributes to the creation of more robust civil societies.

The Caribbean is hardly unique in facing governance issues. According to the World Economic Forum, the global cost of corruption in 2018 was estimated to be $2.6 trillion. In recent years, international news has been rife with headlines of corruption in high places. In Malaysia, the 1MDB scandal helped bring down the government and put its former prime minister on trial for corruption.

Moreover, in 2020 the U.S. investment bank, Goldman Sachs, reached a settlement of $3.9 billion with the Malaysian government for its part in the scandal. In Brazil, the 2010s were rocked by Operation Car Wash (Lava Jato), which revealed extensive money laundering and bribery involving the state-owned oil company, Petrobras. The ripples from that scandal ultimately sent one former president to prison, helped impeach another, ruined the reputation of one of the country’s largest and best-known companies, Odebrecht, and snared high-ranking political figures in other parts of Latin America.

The United States also saw its share of public corruption. It is often forgotten but it was only in 1883 that the U.S. officially did away with the spoils system with the Pendleton Act. Even since then there have been many financial scandals—not necessarily involving the government—but nonetheless causing damage to the public faith, including the Savings and Loans scandal, Enron, and Bernie Madoff.

Another governance rating database is the World Bank’s Worldwide Governance Indicators (WGI). This covers a wide range of indicators related to governance and corruption. The World Bank’s program includes items such as “control of corruption” and “voice and accountability”. Under the first are considerations like corruption among public officers, public trust of politicians and transparency, accountability, and corruption in the public sector. Under “voice and accountability” are items such as press freedom, human rights, the role of the military in politics, and openness of the budget process. Another part of the global accountability regime is ESG standards.

Private investors use ESG to gauge how a company or project meets these standards, either through green bonds or direct investment. ESG now accounts for billions of investment dollars and, in the post-COVID-19 environment, is projected to expand further. Moreover, many of the world’s leading companies—a number of them active in the Caribbean—are adopting ESG standards.

According to a KPMG survey, 75 percent of the largest 100 companies across 49 countries indicated that they are employing ESG business models or incorporating aspects of sustainability approaches. This 2017 number indicates substantial growth from just 12 percent in 1993. For Caribbean governments, ESG’s importance is abundantly clear. Investors may shy away from investing in companies operating in countries that have poor track records with environmental compliance, governance, and transparency. This is particularly critical for companies operating in the extractive industry sectors, which have encouraged the adoption of Blue Economic policies that tap the potential of the local ecosystems to add to a widening ESG investment menu.

Considering the competition for international capital, this trend could provide Caribbean countries a wider platform to attract foreign and domestic investment.There are other ways that Caribbean countries and territories are rated. These include organizations like the Organization for Economic Cooperation and Development (OECD), the Financial Action Task Force, and other multinational groups. These create “blacklists” and “greylists” for jurisdictions that are regarded as facilitating financial crimes or tax evasion. The European Union’s Economic and Financial Affairs Council maintains a list of “non-cooperative” jurisdictions for tax evasion.

The last revision, in February 2020 included the following Caribbean countries: the Cayman Islands, Panama, Trinidad and Tobago, and the U.S. Virgin Islands. Jurisdictions that were previously on the EU blacklist were Aruba, Barbados, Belize, Bermuda, and Dominica, but they were removed as they worked with the EU to improve their tax compliance standards.The stakes for the Caribbean are high in terms of governance, especially because the COVID-19 pandemic highly affected the region. The Caribbean already has a number of reasonably well-developed organizations, including CARICOM, the Caribbean Court of Justice, the Caribbean Development Bank, and Caribbean Financial Task Force.

Although there are often complaints over their value, the region would be much poorer without these organizations. They provide important forums for discussion, technical expertise, and the creation of regional standards. Moreover, they reinforce ideas about the need for robust civil societies and their projects help promote civic organizations throughout the region.Looking ahead, good governance and tackling corruption are important to the Caribbean. This comes in many shapes and forms, but for governments in the region to deliver the package of goods their citizens expect—law and order, functioning public utilities, and working healthcare and educational systems—there has to be a commitment to maintaining systems that promote the public good.

This means not just having laws on the books, but enforcing them. At the same time, Caribbean governments have to be aware that as citizens hold them to a higher standard, they are also being held to international standards. Accountability to both domestic and international constituencies may add to an already long list of pressures, but the results are more inclusive and equitable societies—a goal to which all citizens can aspire.

Caribbean economies, which have struggled to recover from the 2008 – 2010 financial crisis, have been particularly hard hit by Covid-19 and the resulting economic fallout.Increasing focus on the region by the U.S. due to its economic, social and security significance is heightened by major oil discoveries and Chinese interest in the region.

Massive flows of ESG capital could aid in remaking the region, financing a new economic model built on technology and improved infrastructure.An old-fashioned oil boom will also contribute significantly to growth, particularly in Guyana, Suriname and Trinidad & Tobago.With all of these powerful economic drivers converging in the Caribbean, it is time for investors to take note of the region.

While there remain challenges, the nations of the Caribbean understand that embracing technology, such as blockchain, along with upgraded communication infrastructure are essential keys to catching up with the rest of the world. This presents both opportunity for international investors and will itself be a significant driver of future economic growth in the Caribbean.

ESG & SDG Investment

Investing in accord with “environmental, social and governance” (“ESG”) principals and “sustainable development goals” (“SDG”) of the United Nations is here to stay. According to an article by the Chief Economist of the Inter-American Development Bank ESG dedicated investment funds account for more than $20 trillion, or one-quarter, of professionally managed assets world-wide.This includes the Caribbean as part of a larger discussion of Latin America and is convincing in its argument that the focus of major international development institutions in facilitating ESG and SDG investment in both the Caribbean and Latin America represents an entrenched, long-term trend.

ESG and Impact Investing in Africa

FOCUS ON NIGERIA AND SOUTH AFRICA

A strong end to 2020 was boosted by factors including the US’ announcement of a further $1.9trn of Covid-19 related stimulus, the challenge for emerging markets investors now is to focus on five years of real change across economies.

On a global scale, emerging and frontier markets account for the largest share of the world’s population, land and mineral resources. They are the drivers of global growth and consumption. Sustainability is a function of their development, and it is therefore essential to promote responsible business practices, enforce human rights and environmental protection.

These are also high impact markets where a minor change can have major global consequences. Stopping deforestation in Brazil, reducing emissions in China, eliminating poverty in India, or finding a solution to water scarcity in Africa, for example, could change the entire planet. Environmental, Social and Governance (ESG) considerations are vital when investing in developing countries, and if the next five years are to be the years of emerging and frontier markets, they will also be the years of ESG.

Emerging markets funds must use the next five years to ensure ESG is at the centre of investment philosophies, with the biggest environmental and social challenges located in the countries they invest in. Sustainability is a function of emerging markets development, and it is therefore essential to promote responsible business practices, enforce human rights and environmental protection.

NIGERIA

Nigeria is leading the way in impact investing in West Africa where twenty-eight impact investors are active in the country. Over the last few years, impact investments have continued to grow in Nigeria.

TYPES OF IMPACT INVESTMENT

The opportunity for impact investments varies and investors may choose to put their money into emerging markets or developed economies. There is no hard and fast rule on the delineation as to what is and what is not impact investment.

However, Impact Investments span across number of industries including:

- Healthcare e.g., developing and providing technology that will enhance good health of humans, telemedicine/telehealth/e-health

- Education e.g., emerging online education and schools especially during and post-COVID

- Energy, especially clean and renewable energy

- Agriculture

- Microfinancing e.g., digital microfinance banking platforms.

- Housing

LEGAL FRAMEWORK/REGULATORY REGIME FOR IMPACT INVESTMENT IN NIGERIA

In Nigeria, there is no law whose sole purpose is to particularly regulate impact investments. However, there are several laws with implications for impact investment and investors. They include:

- The Companies and Allied Matters Act

- The Nigerian Investment Promotion Act

- The Investments and Securities Act

- Consolidated Rules and Regulations of the Securities and Exchange Commission

- The Finance Act

- The Foreign Exchange (Monitoring and Miscellaneous Provisions) Act

- The Industrial Inspectorate Act

- The Industrial Development (Income Tax Relief) Act

- The National Office for Technology Acquisition and Promotion Act

- The Rulebook of The Nigerian Stock Exchange 2015

- The Immigration Act

Considering the many government institutions that one will have to deal with towards obtaining relevant certifications, permits and or licences, the Nigerian Government, through the Nigerian Investment Promotion Commission (NIPC), created a One-Stop Investment Centre (OSIC) to help bring together all the relevant regulatory bodies and institutions that one may need to relate with for the purpose of obtaining the relevant certifications and or licenses before commencing operations in Nigeria.

The idea behind the creation of OSIC is to help investors (including impact investors) conveniently set up their businesses in Nigeria. How well this aim has been achieved is in doubt.

A CONSIDERATION OF THE CONCEPT FROM THE NIGERIAN PERSPECTIVE

Nigeria, being a developing country in the third world, has its fair share of socio-economic challenges ranging from poverty, hunger, unemployment, illiteracy, lack of (and sometimes, inadequate) social amenities, security, etc. Issues of climate change (being a general problem world-over) also pose a challenge to the country. These challenges are natural attractors of impact investors both within and outside Nigeria.

Hence, the obvious intervention being carried out by some of these impact investors in some of Nigeria’s sectors. Examples of such investors are Uber, Bolt, Gokada, Oride (all car and bike hailing services mostly operational Nigeria), Learners Corner International Limited (a Nigerian Company that uses technology to deliver education to Nigerian Children especially as a result of COVID), LifeBank (a startup that works with hospitals round the clock to find lifesaving medical products and deliver same to the hospitals in the right condition across Africa), Wecyclers, (a company that offers convenient household recycling services using a fleet of low-cost cargo bikes), Andela(a technology company that recruits and trains local software developers at little or no cost, who in turn work remotely for them for various international companies, thereby generating employment opportunities for thousands of the unemployed populace in Nigeria), and the many Agritech Firms (e.g., Farmcrowdy) that use technology and crowdfunding in furthering their existence and objectives.

Furthermore, a good number of impact investing funds have been made available by some foreign development institutions and bodies. For instance, the African Development Bank invested in the Africa Food Security Fund (AFSF) to boost agribusiness SMEs and enhance food security in some African countries like Nigeria. Also, the International Finance Corporation made an investment in Hygeia Nigeria Limited to improve the healthcare infrastructure in Nigeria and to facilitate access to quality healthcare services.

Locally, the Nigerian Capital Development Fund (NCDF) launched an Impact Investment Note and Fairshares investment platform to enable impact investors make investments and become stakeholders in NCDF with the aim of driving sustainable impact projects in the country.

Notable Points

- Nigeria is a country faced with an avalanche of socio-economic challenges like hunger, poverty, unemployment, poor healthcare, poor/inadequate infrastructural facilities, illiteracy, among others, which largely affects its growth and development.

- Data from the National Bureau of Statistics reveals Nigeria’s unemployment rate as at the second quarter of 2020 to be 27.1 per cent indicating that about 21.7 million Nigerians remain unemployed.

- In 2019, The National Bureau of Statistics (NBS) released its “2019 Poverty and Inequality in Nigeria” report, which highlighted that 40 percent of the total population, or almost 83 million people, live below the country’s poverty line of 137,430 naira ($381.75) per year.

- However, these challenges create an opportunity for impact funds and impact investment.

- Over the last few years, impact investments have continued to grow in Nigeria. Its impact, however, might not be significant amidst the plethora of challenges faced across the country. This myriad of challenges impedes the expansion and maximum realisation of its potential to deliver social, economic and environmental returns at scale.

- Nevertheless, these perceived challenges should not serve as an excuse to bury the idea of impact investment. On the contrary, it is a time for stakeholders to re-evaluate guiding principles and collaborate to build a strong socio-economic society.

- For investors willing to bear the risks and challenges, Nigeria holds enormous promise. Its sheer size and strong growth prospects position it well to continue its role as a leading economic powerhouse on the African Continent. Moreover, the large proportion of its citizens underserved by basic goods and services provide a wide variety of opportunities for both financial and social/environmental impact.

LIMITING FACTORS/CHALLENGES TO IMPACT INVESTING IN NIGERIA

While it is clear that impact investments have helped to strengthen Nigeria economically and social wise, several challenges still militate against the continued growth of impact investment. Highlights of some of such militating factors are as follows:

- Difficulty while sourcing for viable investments: Meeting both financial and environmental/social objectives are proving difficult. This is as a result of limited capacity of sustainable social enterprises in Nigeria. Low deal flow is partly due to the limited number of sustainable social enterprises or impact investees able to demonstrate a sufficient track record and capacity development following the risk appetite of impact investors. This is coupled with limited ability to measure and report adequately on impact performance where such capacities do exist.

- Difficulty Exiting Investments: Value in private equity investments in the traditional financial markets is sought and realised through an exit point at which the investor sells their stake in a firm. This can be done through Initial Public Offerings (IPOs) as the endpoint of the funding value chain. The challenge of finding profitable and varied exit options stems from the fact that most African capital markets are still at a relatively early stage of development.

- Unclear Policies and Regulatory Environment: While Nigeria was reported by the World Bank to have improved its ease of doing business in the World Bank Report of October 2019, the issue of uncertainty in policies (almost always a consequence of state politics) and regulations has hampered the development of impact investments. Currently, Nigerian enterprises are generally challenged by a poor environment for doing business, and investors constrained by our developing financial markets.

- Lack of Ecosystem Synergy: There is a poor synergy between sustainable social enterprises, entrepreneurs, investors and innovation networks. The majority of Nigeria’s sustainable social enterprises are not members of professional associations or other formal networks, which makes finding investible enterprises and entrepreneurs a challenge for investors. Furthermore, sustainable social enterprises may have limited access to academic and research institutions focusing on research and development (R&D) that can be developed into goods and services for markets.

- Negative perception: about the unprofitability of impact investing.

THE WAY FORWARD/SOLUTIONS

It is proposed that the following be adopted as solutions towards some of the problems identified above:

- Enacting of an all-inclusive and targeted legislation for impact investors and investment.

- Setting up modalities for proper integration of social enterprises into one umbrella body for easy identification of investors.

- Setting up avenues (like associations and a regulatory body) for education and disabuse of negative and untrue mindset pertaining to impact investment.

- Establishing a central data system to provide information on impact measurement and tracking and other indices emanating from impact investment. This will enable impact investors and other stakeholders make informed decisions and choices.

- Enable and continue to enhance the ease of business operations through means such as adopting tax free regimes or reduced tax obligations for impact investors.

With the great human capital that Nigeria possesses and the numerous economic social challenges, it can be argued that the country is a fertile ground for impact investors and investments. Impact investment is indeed a goldmine whose potential remains largely untapped. Therefore, government and other stakeholders should endeavour to do the needful towards establishing the apparatus needed.

SOUTH AFRICA

Four trends have emerged as South African companies contemplate post-pandemic recovery: new thinking on talent and skills retention, embracing technology, incorporating sustainability in business models, and investing more in employee well-being, benefits and engagement. These were the findings from the South African edition of Mercer’s Global Talent Trends 2020-2021 report, released in March 2021.

The four trends that South Africa companies should adopt are embracing a new multi-stakeholder model that encompasses transparency and empathy; reskilling to transform the workforce for a new world economy; harnessing the power of data and redesigning the work experience to inspire and invigorate employees.

According to the report, 75% of HR leaders in South Africa who participated in the survey expected Covid-19 to negatively affect their businesses. Defining future workforce needs and sustainably restructuring and reinventing should be top priorities for 2021, if companies and organisations are to navigate through the economic crisis sustainably and cost-effectively.

Many South African companies have realised that life will never be the same again post Covid-19. Business survival will, to a large extent, depend on how companies and organisations embrace the future, use technology, invest in skilling and re-skilling employees, develop tailor-made employee benefits, incorporate mental well-being into HR models, develop sustainable working models, and embed Environmental, Social and Governance (ESG) practices in business models.

Up to 67% of the companies surveyed are already building ESG goals into their broader transformation agendas, significantly more than the global average (45%); while one in five organisations (20%) are embedding ESG metrics into executive scorecards.

As a result, companies and organisations have started deeper conversations on such issues as developing people practices that will endure post the pandemic, finding sustainable flexible employee models which can be used as foundations for growth, or for reinventing the future. Companies are now confronted with unavoidable conversations on how they can use the lessons of the pandemic and use innovation, born out of necessity, to develop a new way of working and plan for reinvention and innovation which will include impact investing.

ESG Regulations in the Middle East

In the Middle East, there is a growing maturity and understanding of Corporate Social Responsibility as encompassing economic aspects of an organisation, as well as environmental and social.

National initiatives like the ‘Year of Giving’ and the ‘Year of Tolerance’ in the UAE, organisations are starting to think about the wider context and implications of social responsibility. More than a potential ‘nice-to-have marketing stunt’, it is recognised as a responsibility monitored by regulatory authority. Environmental, social and governance (ESG) may have played a big part in enabling this shift in perspective.

In January 2004, then UN Secretary-General Kofi Annan wrote to the CEOs of significant financial institutions to take part in an initiative to integrate ESG into capital markets. Since then, ESG has evolved and moved from the sidelines to the forefront of decision-making.

In the last decade, various governments worldwide, including those of Switzerland, France, the UK, Italy and Germany, have enacted over 500 new measures to promote this approach, and players from governments and regulators to capital markets, from businesses to consumers are becoming involved.

ESG disclosures gain momentum

Direct and indirect pressure on corporates and other types of enterprises to make more detailed ESG-related disclosures are increasing, and companies are acting now to establish these.

With ESG, organisations are subject to a set of non-financial reporting. Coupled with increasing investor demands, these new rules could have a profound social and economic impact on companies.

Regulatory authorities, for example, are establishing standards and frameworks to ensure mandatory sustainability reporting. Abu Dhabi Financial Services Regulatory Authority (FSRA) plans to introduce ESG criteria for entities at Abu Dhabi Global Market (ADGM).

Furthermore, as stakeholder expectations increase, companies may be faced with growing pressure to manage risks and are expected to be more responsive. Many of these issues are also partly driven by consumer and market demand, such as the need for energy efficiency.

Engagement with stakeholders is therefore central to an organisation’s sustainability, whether shareholders, customers, employees, the community or non-governmental organisations (NGOs).

Many companies only think about human stakeholders, but they have to consider representing the rights and interests of non-human entities as well, including our natural habitat, which is facing unprecedented risks today.

ESG in the wake of crisis

According to the Global Risks Report 2020, which offers a ten-year outlook of some of the biggest challenges facing us, the top five global risks in terms of likelihood are all related to environmental concerns (the report was published before the COVID-19 pandemic).

The publication sounds the alarm on extreme weather events with major damage to property, infrastructure and loss of human life, failure of climate-change mitigation by governments and businesses, and major biodiversity loss and ecosystem collapse.

These may result in irreversible consequences for the environment and severely depleted resources for humankind, as well as industries.

There could also be several interlinked consequences, as witnessed with COVID-19, which has far-reaching social, economic and environmental impacts. The stock markets have taken a hit, and as productions units are shut down, business activity has slowed tremendously.

Now is the time for organisations to listen to what stakeholders want and to implement relevant policies that will safeguard their interests.

Leading banks such as Emirates NBD, Dubai Islamic Bank, Mashreq Bank, Emirates Islamic and Commercial Bank of Dubai announced relief measures for their individual and corporate customers to deal with the impact of the outbreak .

Food delivery platform Talabat announced contactless delivery to safeguard its customers and prevent the spread of the virus. The UAE government has also announced an AED 126bn stimulus package to reduce the impact on both individuals and businesses in the country.

The emirates of Dubai and Abu Dhabi are also implementing a number of measures to counter the economic impact of COVID-19. These actions aim to reduce the cost of doing business and simplifying business procedures, especially in the commercial, retail, external trade, tourism, and energy sectors.

Al Futtaim Group has said it will make substantial contributions to ease the financial burden of its retail tenants by offering a fund of AED 100m to help affected retail businesses as a result of the slowdown.

Meanwhile, Majid Al Futtaim-owned Carrefour has seen a spike in online grocery orders, which has prompted the company to transform many of its supermarkets and hypermarkets into fulfillment centres to cope with the demand.

Sound leadership can make a big difference at times like this, by giving stakeholders confidence that the company will be resilient through crisis. Regionally, many CEOs have conducted virtual sessions with their employees to convey messages of strength and resilience during this difficult time.

These challenging times prompt societies to better understand organisations’ social responsibility towards employees, customers, and other key stakeholders, based on how well they engage and help them cope in such situations.

In the unprecedented times we live in, ESG is perhaps more relevant than ever. While the regulatory developments in the region are a positive step, there is still room for organisations to better understand and recognise the all-round advantages of environmental and social governance.