Nurole’s interview with Dr Miranda Brawn on launching the UK’s first Black Women on Boards (BWOB) initiative

Dr Miranda K. Brawn talks about launching the UK’s first ‘Black Women on Boards’ initiative, reverse mentoring and how board culture can enable greater diversity and inclusion

Dr Miranda K. Brawn MBA FRSA is a British businesswoman, experienced non-executive director, board advisor, lawyer and philanthropist.

She started her banking career as one of the first women of colour on London’s trading floor and went on to hold a number of senior leadership roles at JP Morgan, Goldman Sachs and other top global financial institutions. She’s held multiple board roles within the public, private and third sectors including the Crownsavers Credit Union, the Black Cultural Archives and Lambeth Council. She currently sits on the board of electric vehicle manufacturer Switch Mobility Limited and The Honourable Society of Lincoln’s Inn’s Investment Committee and Social Mobility Committee as part of the Bar Representation Committee. She is also a Bloomberg News TV and Radio expert contributor.

In January 2016, Miranda launched The Miranda Brawn Diversity Leadership Foundation. Its mission is to eliminate the diversity, equity and inclusion gaps in the professional workplace through education and empowerment for future diverse leaders. The charity launched the UK’s first diversity leadership lecture event series and, in 2021, its first Black Women on Boards” (BWOB) initiative.

There seems to be more talk than ever about diversity at the moment – why does real change still feel so slow?

One of the major obstacles is that inclusion still does not make commercial sense to a lot of leaders, despite the fact that a diverse, open and supportive work culture has been proven to be more dynamic and inspire greater innovation.

Reinventing company culture and changing employees’ attitudes and mindsets cannot be achieved overnight, but is urgently required. These initiatives require significant time and investment to get off the ground and become embedded into company culture. It is also a sensitive and emotive topic that many people would rather avoid.

Where should organisations start?

The focus has to be on action and transparency now. There needs to be a strong and consistent message from the leadership on its commitment to DE&I – without this, the message will become confused and lose momentum. More bravery is required for faster change to take place.

In turn, this strong voice empowers people throughout the business to support one another and embody these messages, which has the potential to transform company culture. Leaders need to be held accountable to deliver on DE&I objectives, otherwise these initiatives can fall by the wayside.

Reviewing and adapting processes to make sure they encourage fairness is an important step on this journey. How companies manage and recruit staff has been proven to stifle diversity.

When did you start thinking about launching an initiative focused on boards?

I have wanted to launch this sort of initiative for many years as there has been an obvious gap at board and senior level management for years.

We wanted to kickstart International Women’s Month by raising the awareness that more needs to be done to hire more women with Black African and Caribbean heritage in the boardroom, especially within publicly listed companies.Our “Black Women on Boards” (BWOB) initiative includes an innovative scholarship programme and reverse mentoring programme with senior leaders.

How important is it to have diversity initiatives aimed at specific groups (like black women) as opposed to say all underrepresented groups?

Because although the number of female directors at FTSE-100 firms has increased by 50% in the last five years, it’s mostly white women.

BoardEx data reveals that only around 3% of female board-level roles are held by women of Black, Asian or minority ethnic (BAME) heritage in the UK’s 350 largest listed companies. These are mostly women from Asian and other minority ethnic backgrounds.

Recent research also highlights that for the first time in six years, there are no Black Chairs, CEOs or CFOs in FTSE 100 companies. There is an urgent need to address this unfair and unjust hiring gap with women and men from a Black African and Caribbean heritage.

Tell us about reverse mentoring and why it is so important.

It compliments our existing mentoring programmes by allowing our current students and alumni to act as mentors to senior leaders. They will share their perspective and experiences and, in doing so, help those leaders think about diversity, equity and inclusion.

This is so important because everyone can learn from each other. It enables better inclusion and improves diversity in the talent pipeline. This improves empathy and mitigates unconscious bias. This also drives culture change and gives leaders the opportunity to stay ahead of the trends through junior employees and mentees.

What practical steps can Chairs take to diversify their hiring processes?

Chairs should be looking at the skill sets that they would ideally want on the board, and then the skill sets they have. By identifying the gaps, they can use this as an opportunity to build in diversity – remembering the inclusion part once board members are hired.

A practical step for Chairs is to simply look in different places. There are numerous leaders like myself who have access to a large diverse network of senior leaders looking for board positions. Tap into these people and their diverse networks. Make sure that recruiters are changing their processes to source diverse candidates. In 2022, you cannot afford to say that you cannot find the diverse talent, because there are great diverse leaders out there who are board-ready, like myself.

As well as hiring, are there elements of board culture that need to change to encourage more diversity?

Research has found that diversity does not guarantee a better performing board – the culture affects how well it performs. Diversity does not matter as much on boards where members’ perspectives are not regularly elicited, respected and valued. To make diverse boards more effective, boards need to have a more egalitarian culture — one that elevates different voices and integrates contrasting insights.

What advice would you give to someone who is thinking about applying for their first board role?

Having a wealth of experience is a clear advantage. But when applying for non-executive roles, only use 25% of your time to detail what you did in the past. Reserve the other 75% to focus on the ‘so what?’. You need to give the most weight to explaining how you will apply your experience to the board and how you will add value.

Be mindful that not everyone on the board has to bring everything. You can offer depth in one or two areas and still be a phenomenal director. You need to pitch what you will bring to that particular board and remember you may contribute in different ways to different organisations.

More importantly, do not give up, and reach out to existing board directors for help and advice. There are a lot of wonderful and supportive board directors who are happy to help you to find your first board role.

Dr Miranda Brawn in Forbes Magazine on ESG including DE&I – 2021

Switching To The Right Approach

The recent appointment of Dr. Miranda Brawn to the position of Independent Non-Executive Director (iNED) at Switch Mobility’s Corporate Board brings together these interlinked strands: carbon-neutral transport solutions, corporate governance, regulatory and risk management, and DE&I and ESG agendas.

In a freewheeling discussion, Dr. Brawn shared her views on how the electric vehicle industry can spearhead DE&I and ESG agendas as part of the larger sustainability charter. She emphasized that electric vehicles, which are inherently carbon-neutral, are the future of mobility and will be key to combating climate change challenges. That said, the mobility ecosystem will need to embrace every aspect of sustainability in order to realize socially, economically and environmentally coherent practices and create real, long-term value.

Talking of the importance of embracing sustainability from a holistic perspective, Dr. Brawn highlighted that ESG-driven investments into clean technology solutions and environmentally conscious practices represent only one side of the sustainability coin. The other is DE&I which leads with socially inclusive and equitable approaches, backed by governance commitments.

Elaborating on this idea, she added that actively encouraging work force diversity –whether in terms of gender or race, disability or sexual orientation – across all levels of the organization, particularly at top decision-making levels, can strengthen resilient & responsible, collaborative & creative, inclusive & innovative growth.

For Dr. Brawn, the idea of inclusiveness extends even further to developing products and services that are suitable for all. This could, for example, inform the designs of next generation vans and buses that can be driven by both men and women and by both old and young. For the perennially driver strapped commercial fleet industry, new vehicle design and technology could encourage a new legion of drivers, young and old, to get behind the wheel. Switch is already working towards this goal with the new vehicle design & engineering of its next generation vans.

Dr. Brawn sees technology as catalyzing other positive social impacts in the form of in-vehicle advanced driver assistance systems and health, wellness and wellbeing features that targeted greater comfort, convenience and safety for vehicle occupants/drivers based on their individual, rather than any perceived collective, needs.

Dr Miranda Brawn is the opening keynote speaker for ‘Women Automotive Network’ on International Women’s Day 2022

Skoda’s Member of the Board, Maren Graef, and Dr Miranda Brawn are just TWO of the fantastic speakers confirmed for next month’s Spring Meetup.

LONDON, UK, February 21, 2022 /EINPresswire.com/ — Skoda’s Member of the Board, Maren Graef, and Dr Miranda Brawn Independent Non-Executive Director of Switch Mobility Ltd are just TWO of the fantastic speakers confirmed for next month’s Spring Meetup (which is being hosted by the Women Automotive Network).

Unlike previous WAN keynote sessions, Maren will be taking to the stage, and hosting an interactive ‘Ask a Leader’ session, where she’ll be answering questions from the audience. Dr Miranda Brawn will be addressing how as an industry, we can ‘drive more women to the automotive boardroom.’

A result of a recent poll (which was taken during the Women Automotive Network’s Winter Meetup in 2021) indicated that “only 30.1% of women in the industry feel as though their career goals have the correct internal support.”

Therefore, at next month’s Spring Meetup, there will be a series of specialist, dedicated career and leadership workshops, personal success stories from automotive female leaders, and… speed networking for ALL attendees, – to drive career goals and support in the industry.

Other speakers include Fedra Ribeiro (COO, Mobilize, Renault Group) who will be delivering a talk on ‘Growing New Mobility Business from a Historical core.’

The event will close with a Panel Discussion focus on ‘Leadership, Career Development, Being a Woman in the Automotive Industry,’ with contributions from Penny Weatherup (People Director, Volkswagen Group United Kingdom Limited), Ella Podmore (IET Young Woman Engineer of the Year 2020; Materials Engineer, McLaren Automotive Ltd), and Katharina Hopp, Senior Vice President Business Team Mobility Solutions, Robert Bosch GmbH.

Sponsors Include: McKinsey & Company, Capgemini Invent, Henkel, Flex, Harman, AkzoNobel, Novelis, Micron, Vitesco, Daimler Truck AG, Audi, Ford. Altair, Leoni, Tuxera, Blue Yonder, ITW, and Skoda.

“We are so excited to hold our annual Spring Meetup event once again,” said Stephanie May, the Women Automotive Network’s Commercial Director, and the Spring Meetup’s organiser.

“Last year, 250+ delegates attended, whereas this year, we’re expecting a much bigger turnout, and we can’t wait to celebrate International Women’s Day once again, to support leadership and diversity in the automotive industry, and to bring professionals closer together,” added Stephanie.

About The Women Automotive Network:

The Women Automotive Network is the fastest-growing platform for automotive diversity and technology discussions, – made possible by their events, content, mentorship scheme, and their rapidly growing community of 8000+ members on LinkedIn.

For more information visit: https://womenautomotivesummit.com

Applications for The Miranda Brawn Diversity Leadership Scholarships 2022/23 now open

PRESS RELEASE: 1ST MARCH 2022

The Miranda Brawn Diversity Leadership Foundation (TMBDLF)’s scholarship application process opened on 1st March 2022.

The mission of this registered charity is to eliminate the diversity, equity and inclusion gaps in the professional workplace by educating, empowering and inspiring out next generation of diverse student leaders. The aim is to make a real difference in the lives of our next generation by giving them a ticket to the lottery of life.

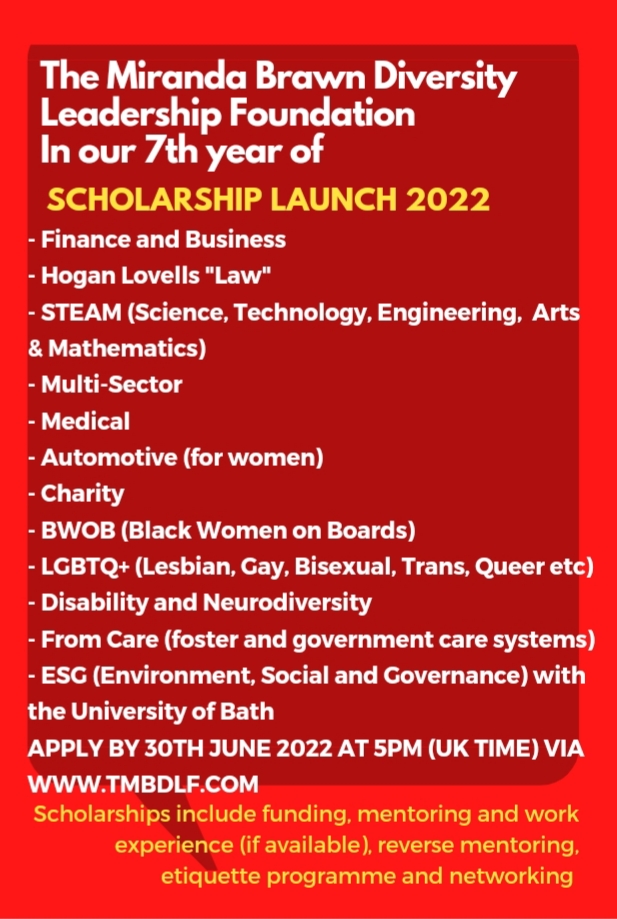

There are at least 12 scholarships available to young people up to ages of 30 years from diverse backgrounds. Set up on the 4th January 2016, this is The Miranda Brawn Diversity Leadership Foundation (TMBDLF)’s seventh year.

Applicants must be at school, college or university on a full-time basis and achieving good grades with an interest in diversity. Applications close on 30th June 2022 at 5pm (London time).

The scholarship award includes £500 to £1,000 in funding, mentoring and reverse mentoring with leaders in their field, work experience (if available and pending COVID restrictions) with leading UK organisations, etiquette educational training, networking, graduation group mentoring lunch and VIP ticket to the annual diversity leadership lectures. More information on the scholarship programme is available via TMBDLF’s website https://www.tmbdlf.com/scholarship-programme.

The categories include Finance and Business, Hogan Lovells ‘Law’, STEAM (Science, Technology, Engineering, Arts and Mathematics), Multi-Sector, Medical, Automotive (for women), Charity, BWOB (Black Women on Boards), LGBTQ+ (Lesbian, Gay, Bisexual, Transgender, Queer etc), Disability and Neurodiversity, From Care (foster and government care systems), ESG (Environment, Social and Governance) with the University of Bath.

Each year we launch new innovative scholarships. This year has included a scholarship called ‘Automotive (for women)’ to celebrate International Women’s Month 2022 and our ESG scholarship has re-launched this year with a University of Bath partnership as part of the One Young World Bath Caucus. Other new innovative scholarships this year include Charity, From Care and Neurodiversity.

A full list of categories and eligibility are also available online. To apply visit the Charity’s website www.tmbdlf.com

The winners will be announced at The Miranda Brawn Diversity Leadership Annual Lecture Event 2022 which will take place later this year in the UK. The date and venue will be confirmed in due course. Further details will be shared on the website by summer 2022. https://www.tmbdlf.com/annual-lecture-and-events

For more information, to support and/or apply for a scholarship, please email TMBDLF’s team directly via info@tmbdlf.com.

Founder Dr Miranda K. Brawn with the Miranda Brawn Diversity Leadership Winners for 2021 at TMBDLF Graduation Group Mentoring Lunch and Etiquette Programme Launch Event held in September 2021 at the Bluebird Restaurant in Chelsea, London UK.